Tiny Home Finance (Australia)

Planning a Tiny Home on Wheels or small dwelling? We map real finance paths — from secured and unsecured loans to asset finance and hybrid structures with land security — then keep negotiating after settlement so savings don’t stop at day one. No broker fee on standard home loans. Video meetings Australia-wide.

Indicative only; final pricing requires a full application and lender approval.

We compare 35+ lenders & specialist options for tiny homes

Updated twice weekly (Wed AM & Fri PM)Eligibility for Tiny Home on Wheels varies by lender and product. We also use specialist personal/asset finance and secured options where appropriate.

Why Rate Challenge for tiny homes

Tiny homes are different. A Tiny Home on Wheels isn’t standard bricks-and-mortar security, and each lender views it through a different policy lens. We assess your plan — Tiny Home on Wheels vs foundation, whether land is available for security, build cost and spec, and your cash flow — then structure the finance so approvals land cleanly and repayments stay comfortable.

Paths we routinely map include: unsecured personal loans for lower-cost shells, asset finance when the chassis and VIN meet policy, refinance with equity release to fund the build, and hybrid structures when you have land security plus a Tiny Home on Wheels. We’ll tell you what’s realistic today, line up the right documentation for your builder, and keep the rate challenge going after settlement.

Want numbers? Use our Tiny Home Finance Calculator for repayments and options. For rules, approvals and council themes, our step-by-step Tiny Home Finance Guide and market context in Tiny Home Industry 2025 — Australia will help you pressure-test the plan.

What you can expect from us

Clear advice, fast triage, and a structure that fits your goals: living tiny on your own land, parking with family, or setting up a compliant granny flat. We coordinate valuation where relevant, builder paperwork, and product selection (fixed vs variable, balloon options for asset finance, fee trade-offs) — then keep banks honest with scheduled reviews.

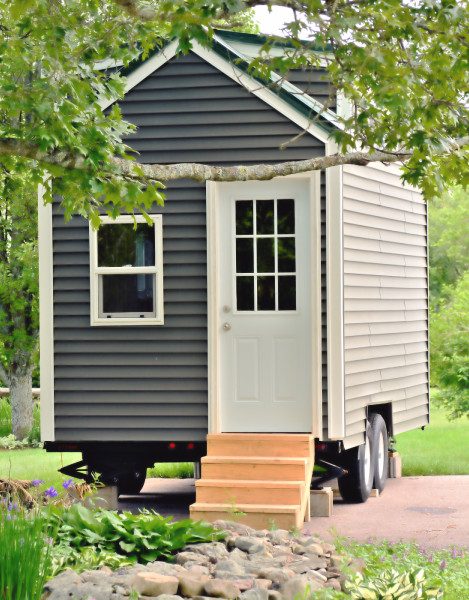

🛠️ Tiny Home on Wheels vs fixed-foundation builds

Tiny Homes on Wheels are often financed via personal/asset loans because they’re movable and don’t create traditional real-property security. Fixed foundations may open up construction/home-loan paths if zoning and building code requirements are satisfied. We’ll explain both — including timing, progress payments and paperwork.

💳 Keeping repayments calm

We model repayments across terms (1–7 years for many asset/personal loans; longer when secured by property) and show how offsets/splits work if you refinance your home to fund the tiny build. Many clients keep repayments steady after a repricing to grow buffers faster.

💧 Release Equity

If you own a property, you can draw on existing equity via a refinance or top-up. This usually delivers the lowest rate, the longest term and the sharpest repayments. Works best when the tiny home will be fixed and adds livability or rental income.

💼 Commercial/Business Loan

Best for eco-tourism cabins, farm stays or staff accommodation. Can be secured (property/business assets) or unsecured at lower amounts. Typical requirement: ABN trading 12+ months. Rates/fees and terms are tighter than home loans, but fit when the use-case is clearly business.

🧾 Personal Loan

The most common option for a Tiny Home on Wheels or smaller builds. Unsecured amounts typically up to ~$75k (sometimes more across multiple loans). Fast to arrange, but rates are higher and terms are short, so monthly repayments are steeper.

🧩 Private Lending

Used rarely when mainstream lenders won’t help. Short terms and higher rates apply with strict conditions. Viable as a bridging step while approvals or income position improve — but we’ll always try to place you with a bank first.

There is no dedicated “Tiny Home on Wheels loan”. Finance is either unsecured, asset/chattel (uncommon) or a land-backed home/construction structure.

Tiny Home tools & guides

Tiny Home Finance Calculator

Estimate repayments and compare loan paths for Tiny Home on Wheels and small dwellings.

Tiny Home Finance Guide

Approval checklists, paperwork, and lender policy themes explained in plain English.

Tiny Home Industry 2025 — Australia

What’s driving demand, common council themes, costs and risks to watch.

What tiny home clients say

Tiny Home FAQs

Can banks finance a Tiny Home on Wheels?

Some do indirectly via personal or asset-finance products; traditional home-loan security is uncommon because a Tiny Home on Wheels is movable. If you have land, we may refinance the property and draw equity to fund the tiny build. We’ll show both paths and the trade-offs.

What documents do I need for approval?

Builder quote/spec with chassis/VIN (for asset finance), proof of income and ID, site or parking plan, and if refinancing: current statements, rates notice and property details. We’ll give you a clean checklist for your scenario.

How much can I borrow for a Tiny Home on Wheels?

Most specialist products range ~1–7 year terms with maximums set by income, expenses and credit history. With property security, borrowing limits are driven by equity, LVR and serviceability. We’ll map the ceiling and a safe buffer.

Can I buy the tiny home now and sort finance later?

It’s safer to structure finance before signing. Some lenders require inspections or specific invoice wording prior to build. We’ll align timing so payments and drawdowns match your builder’s schedule.

Do council rules affect finance?

Yes — policies often ask how and where you’ll live in the Tiny Home on Wheels (primary place vs ancillary). We’ll outline common council themes and make sure your finance path fits the intended use.

Fixed or variable — what do tiny home owners choose?

Asset/personal loans are usually fixed-rate. Refinance paths can be variable with offset for flexibility. We’ll model both so you can pick stable payments or a buffer-building strategy.

Can I use progress payments?

Some products allow staged payments; others pay on delivery. We’ll select the lender to match your builder’s milestones so the build isn’t delayed.

How can I estimate repayments now?

Use the Tiny Home Finance Calculator. We’ll then fine-tune with your exact spec and term.

What about granny flats and kit homes?

If fixed to land and compliant, you may access home-loan or construction products. For relocatable or modular builds, we map alternatives including asset finance and refinance strategies.

What’s the fastest way to get started?

Book a quick triage call. We’ll confirm the viable path, give you a tailored checklist, and set a timeline to approval and delivery.

Visit or book a call

Rate Challenge – Mortgage & Finance Brokers

U 63/17 Armstrong St S, Ballarat Central VIC 3350

- ✓ Open Mon–Fri 9–5 (after-hours by appointment). Video meetings available Australia-wide.

- ✓ 2–3 min walk to Ballarat Station.

- ✓ Same-day triage. Clear next steps after your first chat.

- ✓ Email: admin@ratechallenge.com.au

“Indicative only; final pricing requires a full application and lender approval.”