How mortgage brokers get paid (Australia): commission explained

Most mortgage brokers are paid by the lender when your loan settles and (often) while it stays in place. This page explains exactly how broker commission works, what gets disclosed, how to spot conflicts, and when a separate broker fee can apply — so you can compare options confidently.

Last updated 22 February 2026 • By Rate Challenge – Mortgage & Finance Brokers • General information only (not personal advice)

Looking for a broker with no upfront broker fee on standard home loans? See Free mortgage broker.

Quick answer: how mortgage brokers get paid

- Most residential mortgage brokers are paid by the lender when your loan settles (not by you directly).

- Payment is usually split into upfront commission (paid after settlement) and trail commission (paid over time while the loan remains in place).

- Commission is disclosed in your documents (credit guide / credit proposal / proposal disclosure). You can ask for it in writing.

- A broker should recommend options under a Best Interests Duty and explain trade-offs in plain English.

- In some complex or non-standard situations, a separate advice/broker fee may apply — it should be agreed upfront before you proceed.

If you want the “free broker” version of this (no upfront broker fee on standard home loans), go here: Free mortgage broker.

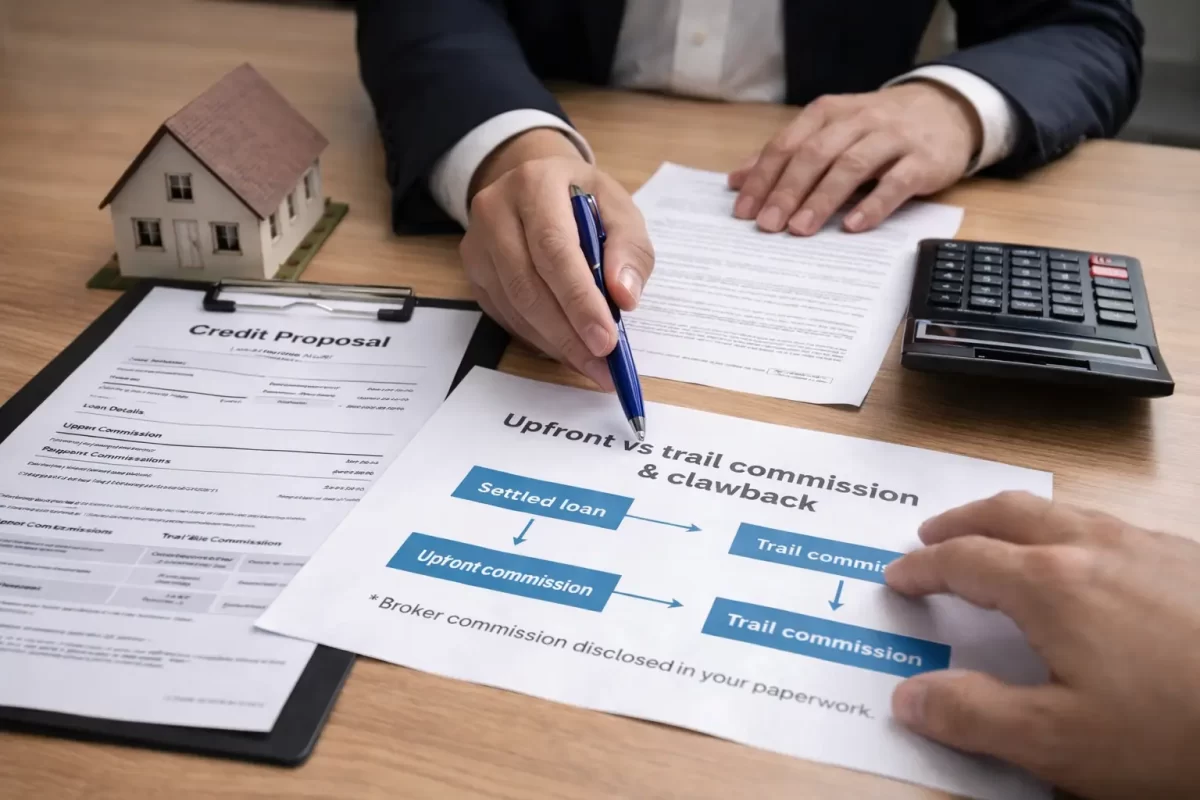

Upfront vs trail commission (and what “clawback” means)

Lenders typically pay broker commission because it’s part of how the lender distributes loans (similar to marketing, branches, or call centres). The exact amounts vary by lender and product, and they’re disclosed in your paperwork.

The key idea is simple: there’s usually an upfront payment after settlement and an ongoing trail payment while the loan remains in place. If the loan is refinanced or closed early, a “clawback” can apply.

| Payment type | When it’s paid | Usually based on | What it means for you |

|---|---|---|---|

| Upfront commission | After settlement | A percentage of the settled loan amount | You don’t pay a “line item” upfront broker invoice on most standard home loans. It’s lender-paid and must be disclosed. |

| Trail commission | Ongoing (while the loan remains) | A percentage of the outstanding balance over time | Trail is intended to support ongoing service: reviews, repricing requests, and helping you adjust your loan as life changes. |

| Clawback | If a loan is closed/refinanced early | Lender reclaims part of paid commission | Some lenders may reclaim commission from the broker if a loan doesn’t stay in place long enough. Good brokers still refinance when it’s in your best interests — but they’ll explain timing and costs. |

💡Why do lenders pay commission at all?

It’s how lenders reach customers outside their own branches and call centres. Commission is one distribution channel. What matters is that it’s disclosed and that the recommendation is made under the Best Interests Duty.

🧾What paperwork shows broker remuneration?

You should be given a credit guide and proposal documents that disclose remuneration. If you want it simplified, ask your broker to summarise the upfront + trail in writing alongside the recommended options.

⚖️When might a broker charge a separate fee?

Some complex, time-intensive or non-standard scenarios can attract a fee (for example certain commercial deals, some SMSF situations, or very small loan sizes). If it applies, it should be agreed upfront before work starts. See: Mortgage broker fees.

Does using a mortgage broker make my interest rate higher?

Usually, no — you don’t automatically pay a higher rate because you used a broker. Lenders set pricing and offers across different channels (direct, broker, campaigns).

- Sometimes pricing is the same across direct and broker channels.

- Sometimes offers differ (e.g., a lender may run channel-specific promos or cashback).

- A good broker’s job is to show the true cost: rate + fees + features (offset, redraw, package fees) + your likely refinance path.

If you’re weighing “broker vs bank”, use this comparison page: Free mortgage broker vs bank.

Do brokers get paid more by some lenders?

Commission can vary by lender and product — which is why transparency matters. In Australia, brokers operate under a Best Interests Duty and should be able to show why the recommended lender and structure suits your goals.

How we keep it clean (practical checks)

- Policy fit first: we match your profile to lender rules before an application (income, property type, postcodes, buffers).

- Options + trade-offs: we explain why one lender is better for your situation (not just a headline rate).

- Written disclosure: you’ll receive documents that disclose remuneration.

- Long-term view: we consider future plans (next property, investment, family changes) — not just today’s approval.

Want the fee intent breakdown? Start here: How much does a mortgage broker cost?

What to check before you proceed (simple checklist)

- Ask for a written summary of the recommended options: rate, fees, offsets, and key conditions.

- Ask how the lender assesses your profile (income shading, living expenses, buffers, property rules).

- Confirm whether any broker fee applies (most standard home loans are lender-paid commission).

- Ask about refinancing costs: discharge fees, potential break costs (fixed loans), and timing.

- Ask how often the broker will do a rate review and what triggers it.

Licensed & disclosed: Rate Challenge ABN 79 956 089 604. Credit Representative No. 567366 under Australian Credit Licence No. 390261.

General information only; does not take your objectives, financial situation or needs into account. Final pricing and approval depend on a full application and lender assessment.

Related pages in the “free mortgage broker” cluster

Free mortgage broker (no upfront fee on standard home loans)

Compare lenders, check policy fit, and get a clear loan strategy — with lender-paid commission disclosed.

Mortgage broker fees: how much does a broker cost?

When a broker is truly free, when a fee can apply, and what to ask before you commit.

Broker vs bank: which is better?

A practical comparison: policy access, approval odds, negotiation, and total cost — not just rate.

Talk to a broker (and ask about commission)

Melbourne • Ballarat • Australia-wide (video meetings)Meetings by appointment. Close to major stations and the legal precinct.

Meetings by appointment. Local support for Ballarat and regional Victoria.

Australia-wide support via phone and video.

Standard home loans are typically lender-paid commission (disclosed). If a fee could apply, we confirm it upfront in writing.

Mortgage broker commission FAQs

💸Who pays a mortgage broker in Australia?

For standard residential home and investment loans, brokers are commonly paid by the lender via commission. In some complex or non-standard situations a separate fee may apply — it should be agreed upfront before proceeding. See also: Free mortgage broker and mortgage broker fees.

🧾What is upfront commission?

Upfront commission is typically paid by the lender after settlement, usually calculated as a percentage of the settled loan amount.

⏳What is trail commission and why does it exist?

Trail is an ongoing payment while the loan remains in place. It’s intended to support ongoing service such as reviews, repricing requests and helping you change loan settings over time.

📉Does broker commission change my interest rate?

Usually not. Lenders set pricing and offers across channels. The right approach is to compare the true total cost: rate, fees, features, and likely refinance path. Try: Rate Review Calculator.

⚖️Do brokers get paid more by some lenders?

Commission can vary by lender and product. That’s why disclosure and Best Interests Duty matter — your broker should explain why the recommended option suits your needs, not just a headline rate.

🔁What is a clawback?

Some lenders may reclaim commission from the broker if a loan is closed or refinanced within a certain period. A good broker will still recommend refinancing when it’s in your best interests, but should explain timing and costs.

👀How can I see exactly what my broker is paid?

Ask for the credit proposal / disclosure documents and a written summary of upfront + trail for the recommended options. If anything is unclear, ask the broker to explain it in plain English.

🧠Where do I start if I want a “free broker” comparison?

Start with our Free mortgage broker page — it’s built for lender-paid commission transparency and standard home loan comparisons.

Information is general and may change. Confirm lender policies, fees and pricing before acting.